Stone Co (NASDAQ: STNE)

Stone Co (NASDAQ: STNE)

Buy an exceptional, rapidly growing Brazilian fintech at a bargain price

What if I told you there is an exceptional, rapidly growing fintech company, and you could buy it at a price lower than what Berkshire Hathaway paid for it?

While the average company in the S&P 500 was doing this:

Stone co went like this:

In this piece, we’ll deep dive into why this company is exceptional, why it can grow rapidly, and why Mr. Market is giving you this rare opportunity.

Summary

Stone co is a leading payments, financial services, and software solutions provider in Brazil that enables SMEs and integrated partners to conduct electronic commerce across in-store, online, and mobile channels. Stone's key competitive advantage is its deep-rooted customer-centricity with a market-leading distribution network and exceptional customer service. This is an industry where regulation changes will cause many new-age players to take share from the incumbents, and stone co will be among the best of the disruptors. This company has been growing revenues at ~55% p.a. since 2016 with strong unit economics. Management is mission-driven, fiscally prudent, long-term oriented, and transparent. Mostly due to short-term headwinds in their credit segment, regulatory changes, an adverse interest rate environment, and an unwarranted short report (more details below), the company is currently available at a bargain price. I believe this ~$5.44bn market cap company can return ~34% p.a. over the next 5 years, not accounting for further optionality.

Important Regulatory events

Before 2010, two players dominated the payments field in Brazil- Cielo (established by visa and 3 Brazilian banks), and Rede (part of Banco Itaú). This duopoly structure led to high prices, low innovation, lack of transparency, and poor customer service. Due to this, the central bank initiated several measures to foster competition in the sector, the main one was eliminating the exclusivity agreements of Cielo with Visa and Rede with Mastercard to open the market up to new entrants. Stone co and Pagseguro, two major payment acquirers today, were able to enter the industry in 2012/2013.

In 2020 the central bank introduced PIX [1] the Brazilian instant payments scheme which enables its users to send and receive payments instantly without the need for intermediaries like stone co (the implication for Stone co is covered later).

In Aug 2021 the second phase of the ‘open banking[2]’ regulation was implemented by the central bank. this regulation enabled the sharing of data between regulated entities. Historically, registration and transactional data of customers was solely with the incumbent banks. Now, with the customer's permission, fintech’s like Stone co and Pagseguro can access this data to underwrite their credit products.

In 2021, the central bank initiated a new regulatory framework for ‘registration of receivables’ which substantially changed this space of offering loans against card receivables as collateral, with the result of fostering competition in this space.

Key sector insights

Brazil has a population of 200mn with 149mn internet users, the fifth largest in the world. 95% of the population has access to the internet via cell phone. Yet, >60mn of the population is still underbanked. [3]

Brazil works slightly differently compared to the rest of the world when it comes to how debit/credit cards are handled. Brazilians, whether paying by debit or credit, will usually pay in installments of two, three months. Merchants usually want to receive payments immediately, and companies like Stone co offer them instant payment and charge a ‘discounting fee’. These are low-risk credit assets that offer high returns.

Business overview

Stone co was founded in 2012 by Andre Street and Eduardo Pontes with a mission to serve the small Brazilian entrepreneur in a better way. Way before it was fashionable, stone co has built its culture to be a deeply customer-centric company. Stone co has created a proprietary, go-to-market business model comprising of three pillars[1].

Advanced end-to-end cloud-based technology platform which they built entirely in-house, to be more user-friendly, overcome long-standing inefficiencies in the payments market, and allow them to design, host and deploy solutions quickly.

Differentiated Hyper-Local and Integrated Distribution- Their ‘stone hubs’ are local operations close to the clients that include an integrated team of sales, service, and operations support staff to reach SMB’s locally, efficiently and build deeper relationships with them.

White-glove, on-demand customer service – This approach combines i) Human connection- which seeks to address the client’s needs in a single phone call. ii) Proximity – they have a team known as ‘green angels’ who offer in-person support to clients within minutes or hours, instead of days or weeks. iii) Technology – through a range of self-service tools and proprietary artificial intelligence to help clients manage their operations proactively, and address merchant needs before they are even aware of an issue.

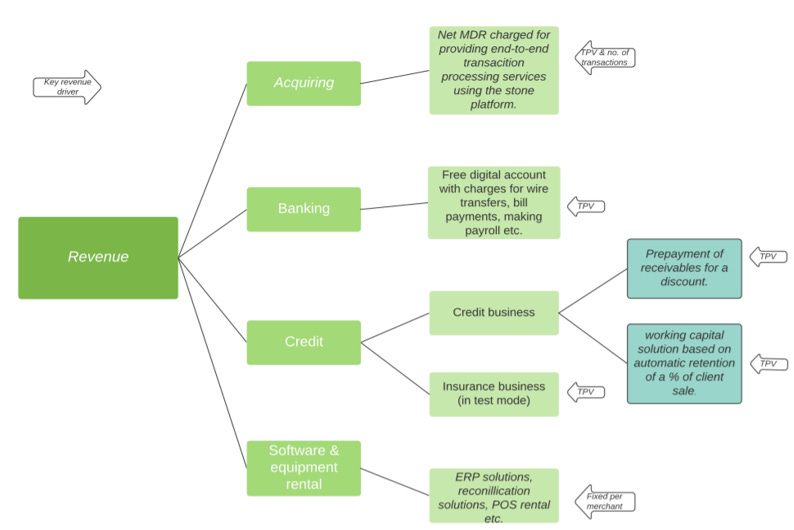

They offer clients a combination of solutions that facilitate in-store, online, and mobile commerce. These can be broken down as follows:

Currently, 72% of their revenue is from payment and financial services to MSMBs and ‘Key accounts’, and 21% is from software services. Within payment and financial services, a significant portion of their revenue derives from-

Merchant discount rate (MDR) they charge on transactions processed through the stone platform.

Prepayment of merchant receivables (Customers in Brazil pay for things in 2–3-month installments, Stone co offers immediate payment to clients and charge a discounting fee).

Competitive landscape

The competition can be separated into three broad categories[1]-

The incumbents- Cielo, Rede, and Getnet.

Major disruptors- Stone co and Pagseguro

Other new-age players – Mercado Pago, Safrapay, Recargapay, Picpay, Nextbank.

71% of the total credit portfolio in Brazil is concentrated among the 5 largest banks3. Due to the regulatory changes, these banks are facing the classic ‘innovators dilemma’ of protecting their gross margins versus innovating and competing with the new age fintechs who have better technology, superior customer service, and more transparency. Stone co.’s NPS score is 65, roughly two times that of the second contender[2] and the four major banks have an average NPS score of 4 [3](nope, that’s not a typo!).

Imagine you start a small business. You want to receive electronic payments. You can order a POS system from stone co and start receiving electronic payments within the same/next day, or you could choose Cielo, and it would take 4-5 working days for the equipment to deliver. If there is an issue with the equipment, Stone co will answer your call in less than 5 seconds (company policy) and solve the problem in the first call about 94% of the time[4], whereas it would take hours/days to handle the same issue with Cielo. You can open a digital bank account with Stone co within 5/6 minutes through your smartphone or you can stand in line at a Cielo bank branch and go through the time-consuming paperwork.

Beyond payments, incumbent banks are still formidable competitors. They offer better credit cards, cheaper loans and are still the trusted primary accounts of most Brazilians. So far, Stone co didn’t compete with incumbent banks for loans. However, with the open banking regulation now in force, fintechs like stone co may have the customer data to underwrite loans for cheaper rates and compete with incumbent banks. Over time, Brazilians may start trusting digital banks to be their primary accounts.

Pagseguro is the main challenger to Stone co. They have slightly different Ideal customer profiles and strategic initiatives. Pagseguro mainly caters to the micro-merchants in Brazil although they are now entering the SMB segment as well. They offer payment, banking, and credit solutions. While Stone co mainly caters to the SMB space, they entered the micro merchant space in 2020 through a JV with Grupo Globo- the largest mass media conglomerate in Latin America. It is arguably easier for stone co to enter the micro merchant space than for Pagseguro to enter the SMB space because these clients require better customer service and proximity to deal with technical problems. Stone co has been building its ‘Stone hubs’ for years to cater to these clients. They are known to have the best sales team and distribution network in the industry.

While many competitors rely on third parties for a portion of their technology, distribution, or customer service, stone co has full control over all these segments to offer superior service. As clients adopt more solutions such as banking, insurance, credit, or software, the churn rate drops by as much as 3x [5]. About half of stone SMB clients are also active in banking, credit, or both solutions. [6]

Why can’t square, stripe, etc. disrupt this sector?

In a podcast episode[1], Augusto Lins (president of Stone co) explained that these companies don’t have a large presence in Brazil because it is expensive for American companies to change their systems to manage the intricacies of the Brazilian payment market. For instance, there is a 30-day grace period for credit cards which must be embedded in the system, plus, consumers pay in installments, so the system should be able to handle that, and in case there is a payment cancellation, and a refund is processed, the system would have to manage this unwinding of installments as well. Of course, stone co also strategically moves beyond payments to build a deeper, more sticky relationship with the customer to avoid this kind of competition.

Key historical figures and events

Stone has grown its total payment volume (TPV) from R$28.1 bn in 2016 to ~R$250bn today, at a CAGR of ~55%.

No. of clients has grown from 82k in 2016 to 1.4 Mn today, at a CAGR of 76%. With nearly 30 Mn MSMBs in Brazil, there is still lots of room for growth.

Net revenue has grown from R$430 Mn to ~R$4bn LTM, at a CAGR of ~55%.

Adjusted net margin increased substantially between 2016-2019 as operating leverage kicked in, and has been lower in 2020 and 2021 due to COVID-19, and other reasons explained in the sections below. Steady-state margins should be upwards of 30%.

They have low balance sheet risk. Their main liabilities are accounts payable to clients which directly flows from accounts receivable from card issuers, as well as their short and long-term obligations to FIDC quota holders which they can pay back just from cash and short-term investments. Their total Debt to equity ratio is 50%.

The historical average take rate has been 1.6% (adjusting for the credit impact in 2021), ARPU is currently R$287, with SMB clients at R$365 and Micro clients at R$117. This is likely to increase as clients use more solutions from Stone co.

They increased their banking engagement, growing this client base to 422k in 3Q21, with rapidly growing money-in, money-out volumes.

Management has achieved this level of growth while maintaining a high level of customer service. Their NPS score is 64. Calls rated ‘excellent’ were ~92% at the time of IPO and now[1]. Their first call resolution is 94%[2].

They have a payback period of 11-15 months for their cost to acquire a client, considering only contribution from payments.

They entered into a JV with Grupo Globo- a leading mass media conglomerate- to reach micro-merchants, who increased from zero at IPO to 545k in 3Q21.

They acquired and integrated Linx in 2021 [3] for a total consideration of R$6.25bn. Linx is a market leader in the retail software segment in brazil with 70k clients across 100k storefronts with R$300mn in GMV, of which Linx currently monetizes only 0.3%. Linx is a sticky business with a 99% retention rate in its core product.

In May 2021, they paid R$2.5bn for a 5% stake in Banco Inter[4] a leading digital bank in Brazil with 10 mn clients, to explore a commercial partnership to maximize the value proposition between banco inter’s consumer and stone’s seller ecosystems.

Adjustments made to net income mostly include share-based compensation expenses, amortization of fair value on intangibles related to investments, and mark-to-market changes to FV of investments in Banco inter. These adjustments are normally insignificant, except for the last few quarters because of changes in FV of banco inter, which I think is an appropriate adjustment as it is out of management control and doesn’t affect Stone co’s economics.

Management

Andre Street and Eduardo Pontes founded Stone co in 2012 having already spent almost a decade building and selling businesses in the fintech space before that. Currently, they are director & chairman/vice-chairman and own ~57% of the voting power in the company. [1] Here’s a little insight into Andre from a former investment specialist at Stone co[2].

“He’s a visionary. He’s our Brazilian Jack Dorsey. Since he was 15 his mentor is one of the richest people in the world. Andre is the kind of guy who launched his first business when he was 14 years old. And he is a very nice guy!”

Augusto Lins is the group president who has been around since the early days of Stone co. He is likely responsible for cultivating the culture of customer obsession in Stone. His book ‘5 seconds’ explains the stone journey nicely. This article gives you a glimpse into his philosophy. Here’s a snippet:

“My calling is to serve the client. I employ 20% to 30% of my time, every day, to talk to clients. Why? To know if they are suffering, to understand their issues, to know how their lives are going. Based on that, we map every situation and adjust our day-to-day routine. I also want to be a role model so the whole company understands that everyone must talk to the client. At Stone, everyone is asked to talk to the client, the fraud prevention team, the data guys, the financial group, because it is fundamental that everyone understands the client's journey and identifies opportunities to innovate, to improve the service and to solve problems. At the end of the day, my purpose is to improve the life of the client further and further.”

Overall, there is good depth in senior management. The chief executive officer, Thiago Liau, and the chief strategy officer Lia Matos are mission-driven, long-term oriented, and transparent. For instance, when the credit problem occurred (explained below), they released a teach-in paper explaining the situation and decided to stop the credit product despite the likely impact on the near-term share price. In 2019, when Stone co.’s share price was falling due to aggressive pricing strategies by competitors, they released a statement explaining how they view the situation. They have been executing good partnerships such as Banco inter and Grupo Globo (though I am not as excited about the Linx acquisition as I will explain later). They seem to be fiscally prudent and focused on the unit economics of their customer acquisition investments. They spent $200mn on buybacks in 2021 when shares were falling, at an average price of $54, suggesting good capital allocation.

A limitation here is that Senior management doesn't own a significant (>1%) a number of shares in the company and is not fiscally aligned with the shareholders.

Stone co is going through a series of headwinds which has seen its stock price plummet ~80% in the last year. You can now buy it at a price lower than what Berkshire Hathaway bought it for at IPO! (Price of ~$24.)

So why is it cheap?

The bear cases –

Credit

The credit offering is one of their main growth areas and management made the mistake of growing too fast in this segment without proper risk controls and taking on too much balance sheet risk. Their accounting method of recognizing revenue upfront using the fair value method instead of the accrual method may have incentivized employees to give out loans without proper risk measures.

This was further accentuated by a regulation change best explained here which led to some merchants and acquirers bypassing a ‘lock’ of receivables created by Stone co as collateral for offering the credit.

This situation hurt Stone co, delinquency rates skyrocketed, and they decided to stop this credit product temporarily in June 2021 for 2 quarters as they obtained more clarity on the new regulation and reassessed their portfolio. There was a R$397.2mn negative revenue contribution [1] from credit in Q2 2021, mainly due to adjustments to credit fair value and significantly lower credit disbursements, which led to a ~13% fall in sequential revenue.

Another argument is that the new regulation will create more competition in the sector. Earlier, only one player could offer credit against a lock of receivables, now with a central registry system, a financial asset will be created, and multiple players can offer credit against the lock of receivables.

Counter-

The issue doesn’t seem structural, rather a setback in what is a major area of growth for Stone co. They plan to soon offer three credit products, with a huge addressable market, this experience will ensure management employs robust underwriting mechanisms to manage risk going forward. They have shifted to an accrual accounting method now and are testing credit solutions that are fee-based with low balance sheet risk. They acquired Gyra+ an SMB lending platform, along with a team of entrepreneurs experienced in credit scoring and risk management. They reportedly brought in a new head of credit as well[2].

Their core prepayment offering is still very lucrative with monthly ROA’s ~2% and low risk as the customer is automatically paying Stone co in installments. In Q3 2021, Their financial income grew 32.1% YOY despite this credit solution going to zero because the prepayment business continues to grow at a rapid pace. They grew SMB total payment volumes (TPV) 104% YOY, with TPV and ARPU both increasing. Their micro merchant segment TON continued to grow rapidly, and engagement in banking increased 4-5x. Overall revenue and income ex credit grew 68% YOY.

Their coverage ratio for non-performing loans stood at 102% as of 3Q21. They have sufficient reserves to cover the losses and meet their liabilities. Management is prudent in their write-offs, and I don’t foresee more provisions going forward.

Regarding competition, while this may lead to a drop in the rates charged by stone co and others, it will increase the total addressable market, and stone's relationship with the clients, their strong distribution network, will allow them to thrive in competition.

PIX & MDR compression –

In 2020 the central bank introduced PIX [3] the Brazilian instant payments scheme which enables its users to send and receive payments instantly without the need for intermediaries like stone co. This solution is gaining popularity rapidly with about 100 mn Brazilians now using PIX. This will challenge stones business as it will affect their ability to charge an MDR on transactions.

Counter-

The popularity of PIX likely brings more people into the financial system than before. This will increase the total addressable market. If I open a bank account to start using PIX, I am also going to receive a debit card, maybe a credit card, or a pre-paid card. I am going to learn more about other financial products. As Augusto Lins said in this interview, “It's not a war against cards, it’s a war against cash.”

This may also detract from new competition in the space. Offering payments was never the end goal for stone. It was the first step to be a trusted partner for their clients. This may no longer be the case for new entrants. Plus, SMBs don’t just want payments, they also require a better experience. They want a system to manage invoicing, inventory and reconciliation as well which stone can offer[4]. Assuming the MDR they charge on transactions gradually falls, I think it will be sufficiently far in the future and they will have enough time to build other solutions to grow their revenues.

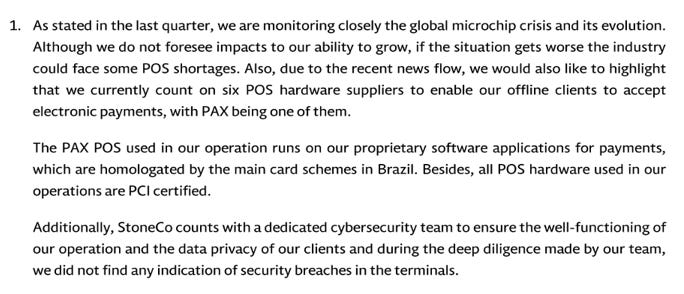

PAX technology issue -

PAX Technology is a Chinese company and a major supplier of POS terminals to Stone co and Pagseguro. The Florida offices of PAX technology were raided by the FBI with sources reporting that the machines have been used as malware droppers and command-and-control locations[5]. Viceroy issued a 2-page short report on Pagseguro and Stone co, claiming they will be subject to significant regulatory action and scrutiny, with the clear possibility of legal action. The report claimed two financial providers had begun pulling PAX terminals.

Counter –

Stone co has approximately 1.4mn clients as of 3Q21, and if we assume they have to replace every single POS terminal, it would cost a little over $50mn according to this article by seeking alpha, a hit to one year's earnings, but not a dent to the long term story.

One small financial provider- FIS’s Worldpay- stopped using PAX because it affected less than 5% of their clients. They sent an email to the US office and didn’t receive an adequate response, so they stopped using the terminals. This tweet by an asset manager does a good job of explaining the situation.

Here’s the response from Stone co which mentions they have six POS hardware suppliers, all the hardware is PCI certified, and in the diligence by their cyber security team, they did not find any indication of security breaches.

Interest rate & profitability-

The base rate in brazil increased substantially in 3Q21, which led to stone co.’s financial expenses to increase by ~4x compared to 3Q20. Compared to the previous quarter it was up ~100%. Interest cost now accounts for ~22% of 3Q21 revenue. Cost of services, selling and administrative expenses also increased YOY and their adjusted net income margin fell to 8.8%, from 45.2% in 2Q2020. Overall, Adjusted net Income was R$128.7 mn in the quarter, compared to R$422.7 mn in the prior-year period.

The ‘adjustment’ includes a major fair value change related to their equity investment in Banco inter, which can be ignored because it is an accounting entry based on a fall in the share price of banco inter, which won't affect the economics of stone cos business.

Counter-

Stone co and Pagseguro have both stated they will be able to raise prices to account for the higher interest rates, but they will do it gradually in a way that doesn’t affect the client relationship. Other than the interest rates, the low adjusted profit margin is explained by i) the R$179.9 impact of the pause of the credit product. ii) R$120 mn in incremental investments in the growth of operations and new business. In my base case valuation model, I am assuming a ‘steady-state’ net margin of ~30% in 5 years. Almost by definition the R$179.9mn and R$120mn are not steady-state charges to profit. Only adjusting for these two the adjusted net margin in 3Q21 is 20%. Assuming management can pass some of the high-interest rates cost to customers (as they have indicated), and the R$120 mn in incremental investments lead to future benefits, as management has demonstrated in the past, then a steady state margin of 30% in 5 years is entirely reasonable.

Software business –

I too am bearish on growth & synergies in the software business because this is not in alignment with their core proposition- the superior distribution channel, customer service, etc. The software market for SMB’s is really small because they are not fully tax compliant as the solution from stone co would require them to be.[6] The companies stone co acquired, including Linx, have separate customer service sections not related to the ‘Green angels’ team at Stone co.

Mitigant- Assuming no synergies, the companies stone acquired are decent companies bought at fair multiples that can grow organically. [7] The Linx clients comprise of larger enterprise companies like Burger King and Mcdonald's, and Stone co may be able to increase their TPV through integration with Linx software but this may not be as profitable due to the higher bargaining power of the enterprise clients. This bearish stance is incorporated in the valuation model, where I assume low to no growth for this business. The businesses will still generate cash, as the retention rate for software products is high- ~99% for Linx’s core product.

Middle management –

Former employees have warned of issues in the middle management[8] as Stone has transitioned from a startup environment to more of a corporate culture.

Mitigant – top management is highly competent and seems to be aware of the problems. They brought in a new head of credit recently and acquired Gyra+ -an SMB lending platform- to bring in a more experienced team in the credit segment.

Other risks -

The foreign exchange risk. Even though the company grows its intrinsic value adverse foreign exchange fluctuations could potentially lower the dollar value created.

Their ability to secure funding at good rates for their prepayment/credit business.

Execution risk of rapid growth, including risks of value destructive M&A transactions.

Supplier concentration risk as PAX is a major supplier of POS terminals for them

Here’s a snippet of the top 5 buyers and sellers during the previous quarter along with this holding as a % of their total public portfolio. [1]

If we think of the percentage of portfolio invested to be loosely related to the depth of research, then clearly the buyers must be on the right side of the metaphorical table.

The bull case

I am bullish on the company being able to rapidly grow their core MSMB client base and sell them credit and banking solutions profitably. I am not suggesting that problems don’t exist, I am arguing that they are overblown, and the opportunity set is still huge.

There are several avenues of growth for Stone co, which are not baked into the valuation model and could offer further upside. Stone co has built a solid relationship over the years in what is perhaps the most profitable client base in the country- the SMB segment- because they have low bargaining power and high service requirements. This client base could provide several monetization opportunities in the future. Their 2Q21 presentation mentions value-added services such as investments, insurance, loyalty and antifraud, additional credit solutions, additional banking solutions such as online sales, payroll, and reconciliation. They can expand into new geographies and sectors, and pursue further strategic acquisitions. I think this is a bet where the risk is baked into the current valuation, and you are getting the optionality for free.

Valuation

The model reflects the fact that I am most bullish on their ability to grow and monetize the MSMB segment, and bearish on the software segment.

For key accounts, they have shifted their strategic focus from sub acquirers to online platforms, and this shift may lead to lower growth in the medium term. Sub acquirers currently represent 40% of the total key accounts revenue.

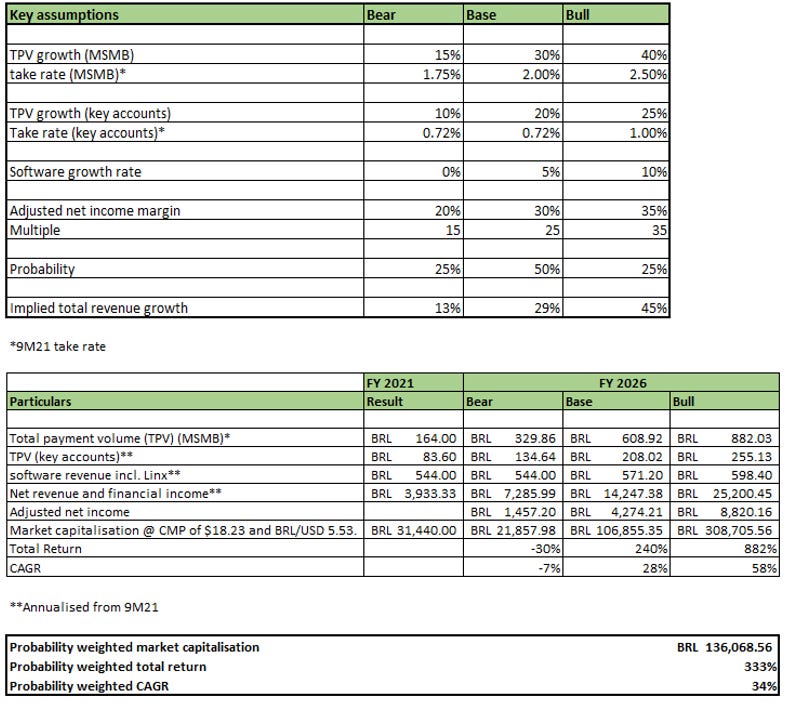

In the bear case, I am assuming competition intensifies and overall revenue grows only 13% as they take some share from incumbents. Their adjusted net margin falls to 20%. Their software business doesn’t grow. Take rates stay the same as new solutions offset lower prices, and the market values it at a multiple of 15.

In the base case, I assume they can successfully grow their MSMB business and slightly increase the take rate through new solutions. The Key accounts business also grows at reasonable rates but take rate stays the same as they have lower bargaining power here. They grow their software business by 5%. They can successfully raise prices to reflect the new interest rate environment, operating leverage kicks in, and they have an adjusted net margin of 30%. The market values the company with a fair multiple of 25x on net income.

In the bull case, I assume they can successfully grow their MSMB segment at high rates of 40% (previous 5-year CAGR was 55%). Take rates in MSMB increase to ~2.5% as they successfully upsell credit & other solutions. The key accounts segment grows at 25% and the take rate increases slightly to 1%, software business still only grows 10% assuming no synergies. They have adjusted net margins of 35% (they have achieved this in the past). The market values the company at a multiple of 35x.

I have arbitrarily assigned a 50% probability to the base case, and assigned an equal probability of 25% to each of the bull and bear cases.

Disclosure: Please do your own research, I am not an investment advisor and this is not investment advice.

[1] https://www.bcb.gov.br/en/financialstability/pix_en

[2] https://www.bcb.gov.br/en/financialstability/open_banking

[3] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Fapi.mziq.com%2Fmzfilemanager%2Fv2%2Fd%2Fd1c190f7-52c1-4663-aa9f-0e0141aa5e3c%2F649e6ecc-ee99-4e5e-1403-d374325e5a46%3Forigin%3D1&clen=574471

[1] Shareholding data from tikr.com. LINK

[1] https://seekingalpha.com/article/4466978-stoneco-stne-stock-understanding-turmoil

[2] https://app.tegus.co/app/database/search?companies=5510-STNE&searchBoolean=OR&transcriptId=23969

[3] https://www.bcb.gov.br/en/financialstability/pix_en

[5] https://www.wokv.com/news/local/fbi-jacksonville-homeland-security-agents-investigating-outside-southside-business/BVFSPMUVUJHWRJTX56PSQDXAZ4/

[1] https://investors.stone.co/node/7646/html#i58bb1b8d611549af94f681bec3c4a8aa_903

[2] https://app.tegus.co/app/database/search?companies=5510-STNE&query=andre&searchBoolean=OR&transcriptId=20316

[1] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Finvestors.stone.co%2Fstatic-files%2Feac0365e-a756-4349-a6c6-353d0ce26704&clen=14985495&chunk=true

[2] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Finvestors.stone.co%2Fstatic-files%2F45-ae99-4e84-bbcc-4ab7c8b5fc72&clen=4449747&chunk=true

[3] https://investors.stone.co/news-releases/news-release-details/stone-enters-business-combination-agreement-linx

[4] https://investors.stone.co/news-releases/news-release-details/stone-enters-investment-agreement-banco-inter

[1] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Fwww.lendacademy.com%2Fwp-content%2Fuploads%2F2021%2F10%2FPodcast-319-Augusto-Lins.pdf&clen=130664&chunk=true

[1] https://app.tegus.co/app/database/search?companies=5510-STNE&searchBoolean=OR&transcriptId=20316

[2] Augusto Lins podcast interview (link)

[3] NPS weighted by TPV for the top five largest players in Brazil, excluding Stone (IBOPE in August 2018) LINK

[4] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Finvestors.stone.co%2Fstatic-files%2F45b2a669-ae99-4e84-bbcc-4ab7c8b5fc72&clen=4449747&chunk=true

[5] Expert transcript #2. LINK

[6] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/viewer.html?pdfurl=https%3A%2F%2Finvestors.stone.co%2Fstatic-files%2F1e1e1d60-8f1e-45fb-8a0c-f966786092e3&clen=1698481&chunk=true

[1] https://www.sec.gov/Archives/edgar/data/1745431/000119312518309043/d580263d424b4.htm#rom580263_2abc

Finally, Someone has read it well. Good one

Tanmay,

Thanks for the note. It just shows you have read what Mr. Market is wrong about.

The references you have tagged and started with chrome-extension need to be fixed. It should be URL directly; otherwise, it won't work. In addition, I do not have access to Tegus and hence cannot read the transcripts. Can you please share somewhere else? If not all, just a snippet of the exact text.

Few more things,

Software business-

I think you are underestimating synergy. The goal is to cross-sell Linx customers with STNE products and offer Linx to STNE customers.

Now this ERP, Restaurant/Store/Business management system is SaaS. It is high-margin recurring revenue.

On top of it, the e-comm integration further solidifies the databank into a stone cloud. This will bring analytics to all Linx/Stone customers and fully suit the capability to manage the multichannel store.

Stone processes brazil's 50% internet payments.

The value provided by the acquisition is unmatchable. It will also provide intelligence to Stone on how the customers are operating, what their business looks like overall, trends, their capital requirements, and how the category of business is doing overall.

This is also a healthy stretch on payroll and tax management. This will further bring an excellent cut on payment, SaaS subscription feature usage, etc.

Second,

Inter stake is quite essential. Please watch all three videos of Inter investor day 2021 by turning on captions and translating the caption to an English setting. You will realize why Stone is interested in Inter and what Inter is doing? Inter also has the intention to go on Nasdaq in 2022. I believe Stone is possibly going M&A there, but nothing confirmed.

https://www.youtube.com/playlist?list=PLuZu2Av0_IiPGxFxlzCSpzOsB7676ebGS

Last,

I agree with valuation of base and bull scenario. If this do well for next 5 years, it will be rolling stone of a decade since switching cost, optionality in business, multiple revenue streams, stickiness via superior customer service and unparallelly distribution network will only build great moat.

Feel free to reach me at - dipak8959@gmail.com

Excellent summary. Thanks a lot for this!